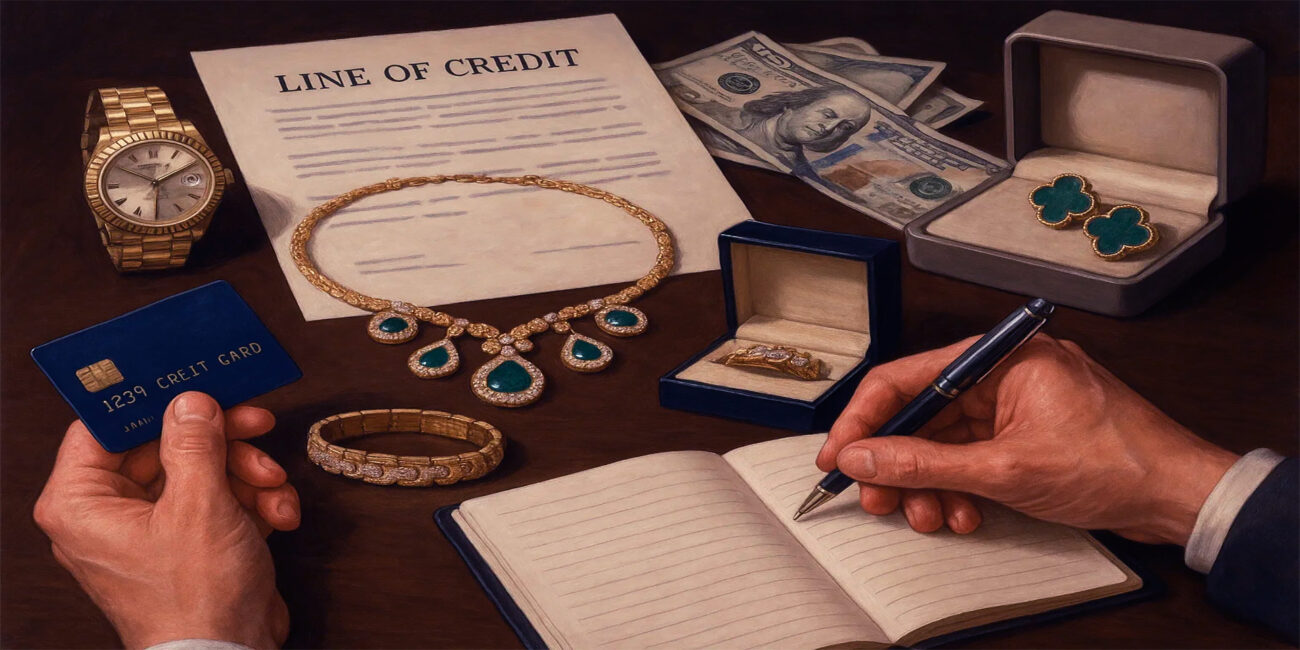

How to Use a Credit Line to Invest in Collectible Jewellery

Collectible jewellery sits at the crossroads of art, luxury, and investment. Signed pieces from Cartier, Van Cleef & Arpels, or Bulgari often carry value far beyond their material cost. Vintage jewels, unique designs, and items with historical provenance can appreciate steadily, sometimes dramatically. For collectors and investors, the difficulty lies not in finding interest but in financing purchases. Auctions and private sales move quickly, requiring immediate liquidity. Credit lines fill this gap. They provide flexibility, speed, and financial breathing room, enabling participation in high-value deals without forcing investors to liquidate other assets. Yet this convenience comes with responsibility. Using credit lines wisely determines whether they become a tool for building wealth or a pathway to unnecessary risk.

Why a Credit Line Works for Jewellery Investment

A credit line differs from a conventional loan. It is revolving, meaning you can draw money as needed, repay, and use it again. For jewellery investors, this matters because opportunities rarely follow predictable schedules. A rare signed bracelet or heirloom necklace may surface unexpectedly. Without access to fast capital, potential buyers miss out. A pre-approved credit line ensures readiness. It also helps preserve liquidity—cash remains untouched for everyday expenses, while borrowed funds cover acquisitions. For dealers, this system creates efficiency, letting them buy stock frequently without arranging a fresh loan every time. For private collectors, it provides confidence to bid at auction knowing financing is secure.

Arranging a Credit Line for Jewellery

Banks, private lenders, and specialized financial firms all offer credit lines suited to luxury assets. The terms depend on collateral and credit history. Property, investment portfolios, or even an existing jewellery collection can serve as backing. Some boutique lenders focus specifically on art and jewellery markets, offering faster approvals and repayment flexibility. Preparation is key. Terms should be negotiated before an opportunity appears, so the facility is ready when needed. Repayment periods, interest rates, and draw conditions must fit your investment style. A collector targeting long-term appreciation may prefer lower rates and extended terms, while a dealer planning quick resales might prioritize fast access with short repayment windows.

Managing Risk When Borrowing to Buy

Jewellery is both valuable and illiquid. Unlike shares or bonds, it cannot always be sold quickly. Borrowing against jewellery purchases adds risk if resale or repayment is poorly planned. Discipline is essential. Clear limits on draw amounts protect against overextension. Insurance is non-negotiable: lenders often require coverage, and it safeguards the borrower against theft or damage. Storage also matters—vaults and secure facilities add to costs but protect investments. Repayment schedules should align with realistic scenarios. For professionals, that might mean resales within months. For private collectors, it may involve gradual repayment supported by other income. Using a credit line responsibly turns it into leverage; using it carelessly makes it a liability.

Mini Case Studies: How Collectors and Investors Use Credit Lines

Case 1: The Opportunistic Dealer

Luca, a dealer in Milan, set up a €500,000 revolving credit line backed by property assets. When an Art Deco brooch collection appeared at auction, he drew €150,000 immediately to secure the lots. Within four months, he sold half the collection to private clients, repaid the draw, and kept the rest of the jewels as inventory. The revolving nature of his facility meant funds were available again for the next opportunity. For Luca, the credit line was not just financing but a cycle—buy, resell, repay, repeat—supporting continuous business growth.

Case 2: The Disciplined Private Collector

Emma, a collector in New York, arranged a secured credit line using her investment portfolio. At a Sotheby’s sale, she used $80,000 from the facility to purchase a signed Bulgari ring. She repaid the draw over two years while enjoying the piece as part of her collection. Her approach balanced passion with prudence—she avoided overspending by setting strict limits and ensured insurance was in place before taking delivery. Emma treated her credit line as a bridge to opportunities, not as an excuse to chase every jewel. Her case shows how discipline turns credit into empowerment.

Case 3: The Overextended Enthusiast

James, a London-based enthusiast, relied on an unsecured line to bid for a rare ruby pendant. Excitement in the auction room pushed him to exceed his original limit. The purchase cost more than expected, and the higher interest rate quickly made repayment difficult. Without resale options, James struggled with monthly obligations. Eventually, he sold part of his existing collection under pressure to service the debt. His experience illustrates the danger of mixing emotion with credit—without discipline, a flexible tool can turn into a financial trap.

Global Trends in Jewellery Financing

The use of credit lines for jewellery investment is growing worldwide. In Asia, expanding wealth has driven demand for signed pieces, with buyers using secured credit backed by real estate portfolios. In Europe, established collectors lean on long-term facilities from private banks, treating jewellery as both a passion and an asset class. In the United States, fintech lenders are experimenting with instant approval systems linked to digital auctions, blending technology with traditional luxury markets. Each region adapts differently, but the common thread is clear: credit lines are no longer rare tools for a select few, but increasingly standard instruments for those who view jewellery as investment as well as adornment.

Future Scenario: Credit Lines in the Digital and Metaverse Era

By the 2030s, jewellery investment may be transformed by digital platforms and metaverse auctions. Imagine entering a virtual gallery where Cartier tiaras or rare diamonds are displayed as high-resolution renderings. A buyer’s digital wallet, linked to a pre-approved credit line, provides instant liquidity. Artificial intelligence analyses credit history in real time and authorizes a draw for bidding without paperwork. Blockchain secures both the loan contract and ownership transfer of the jewel, making transactions nearly frictionless. Decentralized lending pools may also emerge, where collectors borrow from communities instead of banks. These innovations will make access easier but will also raise risks—greater temptation to overspend in immersive environments, exposure to cryptocurrency volatility, and fewer safety nets if defaults occur. Still, for disciplined investors, digital-era credit lines could make participation in high-value jewellery markets smoother, faster, and more global than ever before.

Discipline Defines Success

Credit lines are powerful because they combine speed and flexibility, but success rests on how they are used. The best outcomes, like Luca’s and Emma’s, come when borrowing is tied to strategy and repayment is carefully aligned with cash flow. Failures, like James’s, result from treating credit as limitless. Investors must remember that jewellery, however beautiful, is a long-term and sometimes illiquid asset. Careful planning, insurance, and repayment discipline keep risks in check. Used wisely, a credit line transforms passion into a structured investment path, giving collectors and dealers the agility to seize opportunities without destabilizing their finances. In markets defined by rarity and timing, such agility is invaluable—and in the future, it may be the line that separates those who thrive from those who overreach.